It was 1989-90. An employer, a well-known business magnate, having many business interests in many fields, had paid Rs. 10 as Attendance Bonus to his employees who attended factory on all the 26 working days in a month. The Insurance Inspector (Now, SSO) reported that the employer had not paid contribution on that amount. Notice in Form C-18 (Ad hoc) was issued in 1991-92. The amount claimed as contribution on omitted wages was around Rs. 1600/-.

The employer’s representatives attended hearing and explained their stand. They said that it was not an amount paid as per any settlement between the employees’ union and the management. It was not a bilateral decision. It was an unilateral one and could be withdrawn at any time. It was paid quarterly and not monthly. The employer was, therefore, not required to pay contribution to the ESIC on this expenditure, they said. When asked, pointedly, how the employees were made to understand that they would be paid Attendance Bonus if they had attended factory on all the 26 days, the representatives said that the management had put up a notice in the canteen to that effect, wherein it had also been mentioned that it was unilateral, that it could be withdrawn at any time and that it would be paid once in a quarter.

Final orders were issued under Sec. 45-A, after the hearing was over, determining the contribution payable. Employer’s contentions were recorded and reasons given.

It was explained in the order issued under Sec. 45-A that

- the very fact that the employer had displayed a notice in the canteen proved that the Attendance Bonus had been paid as per specific terms of contract.

- there was an express contract, and that it was not unilateral, because there had been clear communication of mind, the consensus ad idem, and the ingredients of offer and acceptance were there.

- the amount was ‘payable’ every month but was postponed and paid once in three months.

- the amount being ‘payable’ every month, this case fell within the first portion of the definition of the term wages and not within the third portion of it.

Contribution was, therefore, claimed on the entire amount. After a few months, the employer’s representative who came to the Regional Office for some other purpose, said that the CEO had ordered the issue to be challenged in the court of law.

When asked how the CEO expected to win the case, the representative said that the CEO referred the matter to court, because he was paying a standing counsel every month without getting any work done by him. He therefore, wanted to give some work to the standing counsel. The employer paid the dues later with further interest, after the court verdict.

What are those different parts of the definition of the term ‘wages’?  Another major employer did not pay contribution on Conveyance Allowance. When the ESIC asked for contribution, the employer went to court, where his stand was upheld. The judge had reasoned that the ESIC would not have claimed contribution if the employer had given season-tickets to his employees or reimbursed the expenditure. As the employees actually incurred expenditure on conveyance, it was not wages, the Court reasoned.

Another major employer did not pay contribution on Conveyance Allowance. When the ESIC asked for contribution, the employer went to court, where his stand was upheld. The judge had reasoned that the ESIC would not have claimed contribution if the employer had given season-tickets to his employees or reimbursed the expenditure. As the employees actually incurred expenditure on conveyance, it was not wages, the Court reasoned.

But, the fact was that it was not a case of reimbursement. The payment was not in kind. It was an amount paid in cash. The court had traversed the extra mile arguing that the ESIC would not have demanded contribution, if the employer had reimbursed it or had given season tickets. The court had overlooked the fact that the employer had, actually, paid in cash. This fact on record had been ignored by the court. The argument could also be that the employer could have given to his employees grocery, cloth and other domestic requirements too and then paid less contribution only on the remaining carry home pay.

What happened in this case was that our counsel had failed to bring it to the knowledge of the court the first part of the definition of the term ‘wages’ which refers to the payment in ‘cash’. When an amount is paid in cash, the liability to pay contribution arises automatically, unless exempted under the fourth part of the definition of the term ‘wages’. Because, there is no system to ensure that the employee spends a particular allowance only for that purpose.

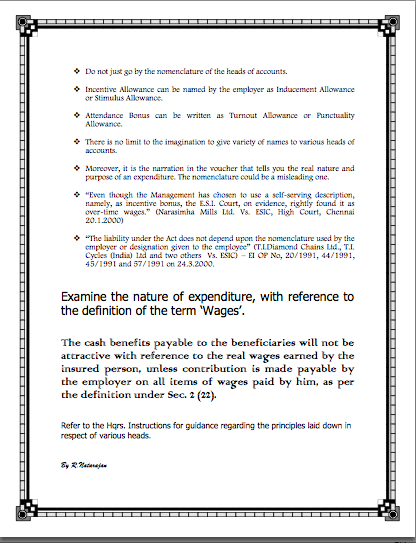

The Act, therefore, does not lay stress on the nomenclature used by the employers to pay remuneration to his employees. ESIC is not obliged to give cognizance to the terminology used by the employer in this regard.  ESIC officers would see only whether the payment fell within the parameters specified in the definition. Many such attempts at evasion to pay contribution had been resisted successfully, only because of the great definition of the term ‘wages’ under Sec. 2 (22). Otherwise, the contribution would have been very less resulting in meager amount of cash benefits to the working population, making it difficult for them to sustain themselves during the period of sickness and disability.

ESIC officers would see only whether the payment fell within the parameters specified in the definition. Many such attempts at evasion to pay contribution had been resisted successfully, only because of the great definition of the term ‘wages’ under Sec. 2 (22). Otherwise, the contribution would have been very less resulting in meager amount of cash benefits to the working population, making it difficult for them to sustain themselves during the period of sickness and disability.

The term ‘wages’ had, thus, been defined in a very thoughtful and foresightful manner in the year 1948. It has withstood numerous onslaughts from various minds with fertile imagination.

Compare this with the contents of Sec. 45 AA which had been drafted very loosely and rushed through as an Amendment in the year 2010 making one wonder whether law-making process in the nation had become so ineffective and inefficient in the nation.

It is time the ESIC turned a new leaf and sent its young officers for training on Legislative Drafting conducted by the ILDR of the Ministry of Law & Justice, to prevent recurrence of such anomalous situations.  NB: The Note in Pdf is available in the following link:

NB: The Note in Pdf is available in the following link: