The concept of Apprenticeship and the need for the Government to give encouragement to that concept can be seen from the Statement of Objects and Reasons of the Apprentices Act, 1961.

Coverage of Apprentices is not permitted under the ESI Act, 1948. For this purpose, the coverage of persons called as Apprentices required deeper examination. Industrial Employment (Standing Orders) Act, 1946 and the Industrial Disputes Act, 1947 refer to Apprentices. After the enactment of the Apprentices Act, 1961, also the ESI Act did not specifically refer to Apprentices. .But, that situation led to ambiguous interpretations and large-scale misuse. The Inspectors were to examine whether there was real training system in the factory, class room, etc., The employers argued that the learners, trainees were also excluded as they were apprentices too. The judgment of the Hon’ble Supreme Court in ESIC vs. Tata Engineering Co and others on October 8, 1975 would throw light on various issues pertaining to the Apprenticeship and the coverage of apprentices under the ESI Act.

“The Apprentices Act, 1850, defines an apprentice as a person who is undergoing apprenticeship training in a designated trade in pursuance of a contract of apprenticeship. Whenever the legislature intends to include an apprentice in the definition of a worker it has expressly done so, for instance, while defining a worker under s. 2 of the Industrial Disputes Act, 1947. The very next year while passing the Employees State Insurance Act, 1948, the Legislature did not choose to include apprentice while defining the word employee. Such a deliberate omission on the part of the Legislature can be only attributed to the well known concept of apprenticeship which the Legislature assumed and took note of for the purpose of the Act.”, said the Hon’ble Supreme Court of India. (http://www.indiankanoon.org/doc/1405877/)

The problems were being encountered in numerous cases at the time of inspections and hearing under Sec. 45. So, the ESI Amendment Act, 1989 addressed the issue and made it specific to exclude only the Apprentices who were covered by the Apprentices Act, 1961 and the Apprentices as per the Standing Orders of the factory (Industrial Establishment).

The ESIC authorities had, however, to examine deeply various aspects pertaining to the Standing Orders and the way in which the Certifying Authority exercised his power to approve those Standing Orders. The Amendment Act, 2010 has put an end to all these problems. Now, only the persons who are Apprentices as per the Apprentices Act, 1961 are excluded from coverage.

But, the ESIC Revenue Manual says something different. The details in this regard are given below for the benefit of readers. They are welcome to offer their views.

Apprentices Act, 1961:

Sec.18: “Apprentices are trainees and not workers –

Save as otherwise provided in the Act, –

(a) every apprentice undergoing apprenticeship training in a designated trade in an establishment shall be a trainee and not a worker; and

(b) the provisions of any law with respect to labour shall not apply to or in relation to such employee.”

Position in the ESIC from 1989:

Sec. 2 (9) of the ESI Act, 1948 says that “employee means …… any person engaged as an apprentice, not being an apprentice engaged under the Apprentices Act, 1961 (52 of 1961), or under the standing orders of the establishment”.

Accordingly, all those appointed as Apprentices under the Standing Orders approved by the competent Certifying Authority as per Sec. 4 of the Industrial Establishment (Standing Orders) Act, 1946 were excluded. But, it was not that simple. The ESIC would see whether the Certifying Authority had really ensured that the Standing Orders were in accordance with the Model Standing Orders. There were cases where the period of training as per the approved Standing Orders was much more than what was permitted as per the Model Standing Orders, both for skilled and unskilled persons. In that event, the ESIC would seek confirmation from the Certifying Authority how he certified and whether he had, indeed, certified those Standing Orders which were produced before the ESIC authorities. In many cases, the Certifying Authorities chose to keep mum, as they had certified those standing orders in violation of the provisions of the Act concerned. In such cases, the ESIC would not accept those employees as Apprentices. The Certifying Authority cannot approve any Standing Order for any factory or establishment, if those Standing Orders are in deviation of the Model Standing Orders.

There were also cases where large number of employees were shown as Apprentices as per the Standing Orders and payment of ESI Contribution avoided. But, in regard to Tamilnadu Region, disproportionate number of employees in any cadre were not permitted to be shown as Apprentices. Contribution was claimed in respect of all persons exceeding 5% in every cadre as ruled by the Hon’ble High Court of Chennai in the Pallavan Transport Corporation Vs. Appellate Authority in the year 1979 . This case was with reference to the provisions of the Industrial Establishment (Standing Orders) Act, 1946. The decision is available in the Book of K.D. Srivastava on the said Act published by the Eastern Book Company.

(1979) 2 LLJ 262

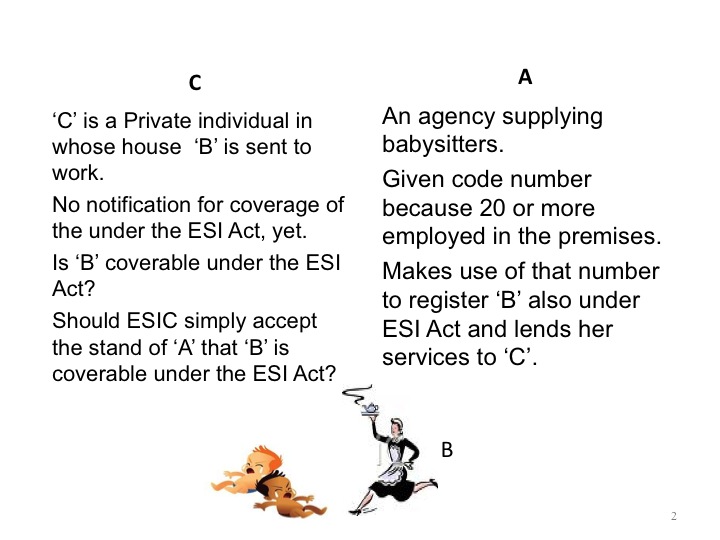

Click on the image to have a larger view

Position in the ESIC from 01.06.2010:

Sec. 2 (9) of the ESI Act, 1948 says that “employee means ….any person engaged as an apprentice, not being an apprentice engaged under the Apprentices Act, 1961 (52 of 1961), and includes such person engaged as apprentice whose training period is extended to any length of time.”

The amendment of 2010 did away with the need to examine the contents of the Standing Orders. All those who are called as Apprentices by the employer are now coverable under the ESI Act, 1948 except only those who fall within the purview of the Apprentices Act, 1961.

What does the ESIC Revenue Manual say?

But, Para L.2.12 in Page 23 of the Revenue Manual published by the ESI Corporation in the year 2011 says as under:

“Exceptions: The following categories need not be counted for the purpose of coverage of the factory or for their own coverage.

…. c) An apprentice engaged under the Apprentice Act, 1961 excluding the Apprentice whose training period is extended to any length of time.”

This is again reiterated against Item 1 under the category “Exclusions” in Page 78 under the Para L.6.4 which reads as follows:

“Exclusions are:

(1) An Apprentice engaged under the Apprentice Act 1961. Consequent to the Amendment to the Act in 2010, only the Apprentices covered under Apprentice Act 1961 are not coverable as employees under the Act. Apprentices engaged under Apprentice Act whose training period is extended to any length of time and all other trainees working under the Standing Orders of the companies are coverable as employees.”

- Does it imply that the ESIC says that the Apprentices engaged under the Apprentices Act, 1961 are coverable, if their training period extends to any length of time?

- Does this not run contrary to what is, correctly, mentioned against Item 6 in Para L.2. 11 in Page 22?

- Is not Item (c) under Para L.2.12 , then, in violation of Sec 18 (a) and (b) of the Apprentices Act, 1961?

- Can the ESI Act, 1948 supersede the Apprentice Act, 1961 on the core issue of the status of an Apprentice, when there is no specific provision in the ESI Act for such supersession?

- Is it not reasonable on the part of the employers to expect clarification from the ESIC authorities with reference to the aforesaid interpretations and discrepancies in the Revenue Manual?